Automatic Exchange of Information

Money moves across national borders with ease

Information about that money should flow just as easily

Money moves across national borders with ease

Information about that money should flow just as easily

As the world continues to globalize, money can move thousands of miles at the click of a button. While this helps facilitate trade, boost connectivity, and allows people to send money to family members around the world, this new global reality also allows illicit money to move with the same ease. Criminals, tax evaders and corrupt politicians get to take advantage of a porous financial system, but government authorities tracking these culprits have to work under the constraint of national borders.

Tens of trillions of dollars are held offshore, and much of this money goes untaxed and unaccounted for. Thanks to the SwissLeaks, which offered a unique snapshot into one of the world’s most secretive jurisdictions, we know that assets that vanish to offshore bank vaults aren’t just a problem for places like the U.S. and Europe. Wealthy elites from all over the world use secrecy jurisdictions to stash assets and evade tax.

In most countries, if a government wants to learn about assets and accounts held by its citizens in another jurisdiction, they must request the information on a case-by-case basis.

This antiquated and tired approach to a fast-moving and global problem makes it difficult to even begin to scratch the surface.

But the problem is particularly severe for low and middle-income countries. It’s estimated that roughly 33% of all assets of the Middle East and Africa are held offshore; for Latin America, it’s about 25%. Globally, that number drops to 6%. Unfortunately, the regions with the highest percentage of assets offshore are the very same regions that would benefit from increased tax revenue to spend on the drivers of development, like roads, schools, and health care.

An Unequal Exchange: our 2017 research with FTC member organization Christian Aid shows that poor countries are being left behind in the global fight against banking secrecy. View the project here.

Thanks to tax havens and an army of lawyers, bankers, and accountants that profit from the secrecy industry, it’s often nearly impossible to find out if someone is evading tax by holding their assets offshore. In most countries, if a government wants to learn about assets and accounts held by its citizens in another jurisdiction, they must request the information on a case-by-case basis. And often before you can even ask for information, you need to know who you’re looking for and where their cash is; coincidentally, this is also the information you are hoping to receive. This antiquated and tired approach to a fast-moving and global problem makes it difficult to even begin to scratch the surface.

To really know the scope of assets held offshore, and to curb tax evasion and illicit flows, government authorities need access to information. Fortunately, there has been some movement on this front. The G20 and the Organization for Economic Cooperation and Development (OECD) have drafted a Common Reporting Standard (CRS) to serve as a foundation for a global network of automatic exchange. The goal is to allow a country to exchange the financial information of foreigners, like names, addresses, tax identification numbers and account balance information, at regular intervals with the account-holder’s home country government.

This is a huge step when it comes to the information governments will have at their disposal to fight offshore tax evasion, but many questions linger about exclusion of the low- and middle-income countries that have the most to gain from a cross-border exchange. The new standard requires a country to participate reciprocally; in other words, to receive information, you have to be able (and willing) to share your information, as well.

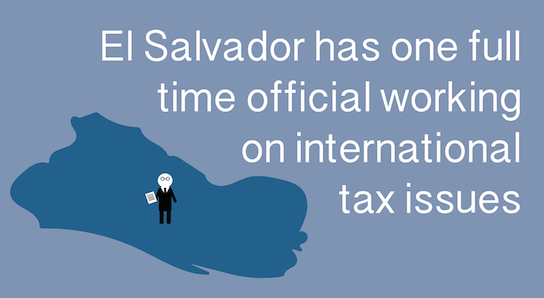

While this requirement may sound sensible, the reciprocity clause is problematic for some developing countries that don’t have the technological capacity or the staff to compile the information. Often, an entire country may have just one or two employees devoted to international tax issues. Sub-Saharan Africa, for example, would need to add roughly 650,000 tax administrators to reach average global staffing levels.

A relatively small amount of money is moving from rich countries to poor ones, yet vast sums are moving the other way, making it only sensible to offer developing countries a grace period where they can receive information without sending their own. It’s quite evident that as the G20/OECD process moves forward, developing countries need to have a larger say in the exchange system.

With an eye on including all nations in a new automatic exchange system, a global automatic exchange system will help give way to a more equitable financial system that’s able to identify the trillions currently held offshore and out of sight.